AUSTRALIAN INSTITUTE OF ENERGY

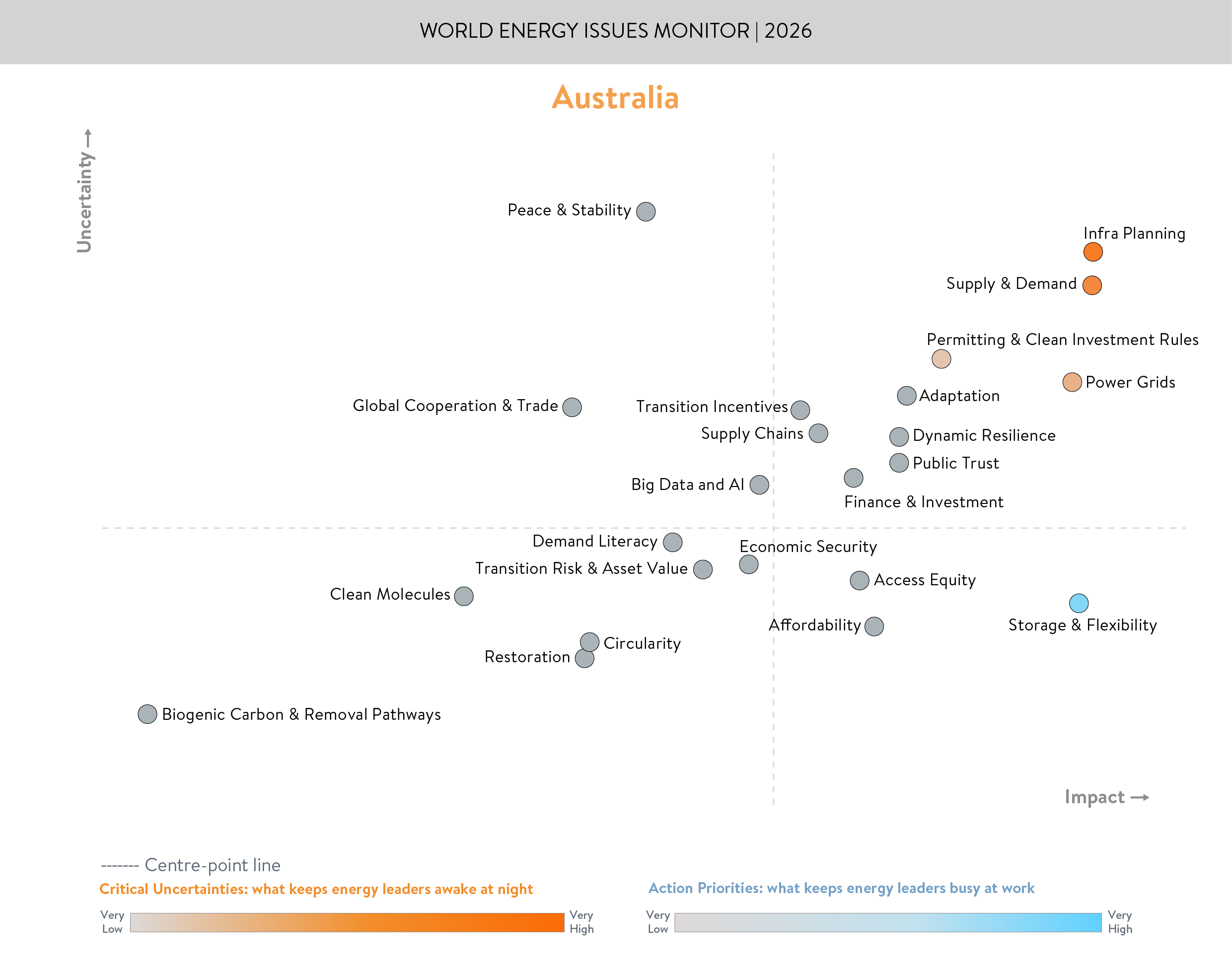

2025 saw a record-breaking year of progress in Australia’s integration of renewable energy, largely variable renewables such as wind and solar. This is reflected in ‘Supply and Demand’ surging to one of Australia's top critical uncertainties, and ‘Storage and flexibility’ remaining the top action priority.

Renewables plus storage supplied approximately 51% of generation in the final quarter of 2025, marking the first sustained period in which clean energy exceeded half of total output. Wind generation increased strongly year-on-year, grid-scale solar continued to expand, and battery discharge nearly tripled. Coal and gas generation both declined over the same period, with coal’s share reaching historical lows as retirements approach. In South Australia, where the last coal plant closed in 2015, the grid reached a world-record of being supplied >40% by utility scale batteries in December 2025. Australians continue to invest in residential renewable generation and storage, with 2025 seeing the proportion of homes with rooftop solar exceed 37%, fundamentally reshaping midday demand profiles. EVs comprised just over 12% of new car sales in 2025, a substantial increase on prior years but still below global averages and many OECD peers.

The issue rising fastest in urgency is ‘Infrastructure Planning’. Renewable capacity commitments continue to accelerate, offshore wind zones are being declared, storage pipelines are expanding rapidly, and industrial electrification is gathering pace. What is hardest to move is the physical system itself. Transmission corridors, environmental approvals, social licence, land access negotiations, grid connection studies and skilled workforce availability all operate on timelines that were designed for incremental change. They are now being asked to deliver whole-of-system rewiring, at pace.

Coal retirements are scheduled across the coming decade (Yallourn in 2028 and Loy Yang A in 2035 – combined circa 50% of Victoria’s electricity, although the Queensland Government has extended major coal retirements until 2046, but has the benefit of underutilised gas peaking plant which can pick up the shortfall) at the same time as load growth is emerging from electrification, data centres and hydrogen pilots. In its 2024–25 system security planning, the Australian Energy Market Operator (AEMO) declared current or emerging system strength shortfalls specifically for New South Wales, Queensland, and Victoria, amidst the withdrawal of these synchronous generators. If transmission and firming development lag behind generation build-out, the result will be curtailment, rising system costs and weakened investor confidence.

Infrastructure risk is already shaping behaviour: developers are prioritising projects with clearer grid pathways, capital is pricing connection risk alongside commodity risk, and governments are reconsidering coordination mechanisms and underwriting tools to smooth delivery – as we’ve seen with the recent National Electricity Market (NEM) review and introduction of the Electricity Services Entry Mechanism (ESEM).

Affordability fell sharply in perceived uncertainty in Australia's 2026 map compared to 2025. Higher renewable and storage penetration coincided with significantly lower average wholesale electricity prices, which fell to around $AUD 50/MWh in late 2025, well below previous peaks. Households with rooftop solar and batteries are increasingly seeing very low or near-zero energy bills, softening cost-of-living pressures for those able to invest. This has helped ease the immediate affordability narrative that dominated previous years. However, this shift introduces new trade-offs. The system must now manage growing divergence between customers who can invest in distributed assets and those who cannot. To this end, in 2025 the Australian government announced a mandatory ‘Solar Sharer Offer’ to require retailers in some states to offer all homes an electricity tariff with a period of free power in the middle of the day, to come into effect in July 2026. Policy choices over the next two years will need to ensure that network and market reforms distribute system benefits broadly rather than concentrating them among asset-owning households. The question is no longer whether renewables can reduce wholesale prices; it is whether the transition can maintain fairness as cost recovery shifts toward network and system services.

Emerging blind spots are ‘Adaptation’ and ‘Transition Risk’ under intensifying climate conditions. Heatwaves are driving evening peak demand higher and more frequently, placing stress on networks during extreme weather events. As coal exits and the system becomes more inverter-based, resilience will depend on firming, storage, flexible demand and robust distribution networks. If adaptation lags, security risks could harden into structural disadvantages. ‘Acceptability’ was a top critical uncertainty last year, but its decline in prominence may reflect the federal election outcome, which provided policy continuity and reaffirmed incentives such as cheaper home battery support. However, lower perceived uncertainty should not be mistaken for guaranteed consent. Transmission development and land use change remain locally contentious. Trust will need to be continually earned through delivery, transparency and tangible community benefit.

Australia’s relative insulation from major geopolitical flashpoints shapes its energy narrative. The country possesses abundant fossil and renewable energy resources and is less exposed to cross-border energy security shocks than many other countries. However, this perceived security presents national blind spots. Australia is not immune to geopolitical shocks as its national gas, oil, and petrol supply are deeply interwoven with global supply chains. A national fuel crisis was declared in March 2026, with the national government expecting affordability to be negatively impacted for the ‘foreseeable future’. Renewable technology supply chains are also global. Utility-scale batteries, solar modules, wind turbines and EVs are predominantly sourced from international markets. A prolonged disruption to global manufacturing or trade flows would materially affect deployment timelines. Energy security in Australia is therefore less about resource scarcity and more about technology access, skilled labour and industrial capability.

The brightest momentum in 2026 is from ‘Storage and Flexibility’. Uncertainty around ‘Power Grids’ and ‘Storage’ declined significantly compared to the prior year, even as ‘Storage’ remained the top action priority. Australia emerged as one of the world’s leading battery markets relative to system size. Approximately 1.9 GW and 4.9 GWh of new utility-scale battery capacity were added in 2025 alone, more than the previous eight years combined. The national project pipeline expanded to roughly 14 GW and 37 GWh near financial close. Household storage surged following the launch of the federal government’s Cheaper Home Batteries Program on 1 July 2025, which offered around a 30% upfront discount through eligibility under the Small-scale Renewable Energy Scheme. Around 175,000 installations were expected by year-end, representing close to 4 GWh of distributed capacity. By late 2025, roughly 4–4.5% of Australian households had a home battery, with penetration exceeding 11% in South Australia. Batteries are now routinely providing both self-consumption benefits and grid services such as frequency control and peak demand management. Western Australia’s state program has linked public funding to virtual power plant participation, and aggregation models are maturing across the country. The national Capacity Investment Scheme is incentivising industry to develop energy in zones that are critically important to the national grid through guaranteed offtake arrangements, which has been highly successful in driving investment in both generation and storage. Storage is easing the sustainability-security tension by firming renewable output, while also supporting affordability through reduced wholesale volatility.

Demand flexibility is advancing in parallel, albeit somewhat responsive to consumer-led adoption of Distributed Energy Resources (DER). Energy Ministers ratified updated roles and responsibilities under the national Consumer Energy Resources Roadmap, clarifying evolving Distribution System Operator (DSO) functions to coordinate two-way energy flows. The Australian Energy Market Operator strengthened distribution-level visibility and forecasting in preparation for the 2026 Integrated System Plan, improving the modelling of rooftop solar, batteries and flexible demand. Dynamic export technology for rooftop solar, enabled through the national Common Smart Inverter Profile (CSIP-AUS) interoperability standard, expanded beyond early adopters, allowing networks to manage exports in real time rather than imposing static limits. A national test and certification capability for CSIP-AUS was established, and the National Energy Public Key Infrastructure body was introduced to provide secure authentication for DER communications. These developments signal a shift from simply connecting distributed resources to actively orchestrating them. Flexibility is moving from concept to embedded system architecture, although peer to peer, virtual power plant, and V2G energy sharing schemes are largely nascent initiatives within an emerging regulatory environment.

‘Permitting and Licensing Delays’ appear somewhat less prominent than in the previous year, but coordination challenges remain. The transition is increasingly about sequencing rather than ambition.

While Australia is targeting 82% renewable electricity generation by 2030, can policy alignment, capital allocation and community consent move quickly enough for renewables and storage to outpace coal closures without eroding reliability? And will large-scale public investment in household batteries strengthen the overall grid for all customers, including those without assets, or unintentionally widen inequality? Australia enters 2026 with strong momentum, declining uncertainty around storage and grids, and falling wholesale prices, alongside several parallel market reviews and reforms. The next phase will test whether institutional coordination, social licence and equitable design can keep pace with technological acceleration.

Acknowledgements:

Australia Member Committee, World Energy Council

Downloads

Australia World Energy Issues Monitor 2026 Country Commentary

Download PDF

World Energy Issues Monitor 2026

Download PDF

Australia World Energy Issues Monitor 2025 Country Commentary

Download PDF

World Energy Issues Monitor 2025

Download PDFLatest Publications

World Energy Issues Monitor | 2026

Published on 26 March 2026

Powering the Global Mutirao: A Call to co-design more and better energy systems together

Published on 08 November 2025

2025 Global Energy Scenarios Comparison Review

Published on 03 June 2025

Latest News