The BusinessNZ Energy Council (the ‘BEC’) is a multi-sectoral group of New Zealand business, government and academic organisations taking on a leading role in creating a sustainable energy future for New Zealand. Since 1 January 2013, the BusinessNZ Energy Council brings together the memberships of BusinessNZ and the former Energy Federation of New Zealand. The BEC shares energy information, represents the views of its members, promotes dialogue and networking for its members, prepares and disseminates reports and organises seminars and conferences. Its goal is to “support New Zealand’s economic well-being through the active promotion of the sustainable development and use of energy, both domestically and globally.”

Greg was previously CEO of the Beca Group from 2012-2023, one of largest privately owned professional services consultancies in the Asia-Pacific region with 4000 staff based in eight countries. Greg provided strategic leadership to all operating geographies as they delivered client projects in typically 45 countries every year. An employee-owned business, Beca is a NZ headquartered multinational that has delivered innovation for its clients for more than 100 years. As Managing Director for Beca Australia from 2006-2012, Greg oversaw the delivery of the $4B Victorian Desalination project, Beca’s largest design commission and which delivers around one third of Melbourne's water supply.

Greg previously held senior management roles in asset management and information technology consultancies. His early career with the NZ Navy culminated in senior roles covering operations, policy and major project delivery. Greg is an Officer of the NZ Order of Merit, a Fellow of Engineering New Zealand, a Chartered Member of the Institute of Directors in New Zealand and holds a Masters degree in Engineering and a First Class Honours degree in Mechanical Engineering from the University of Auckland.

Greg is also the NZ Co-Chair of the Australia-New Zealand Leadership Forum and Chair of the NZ Defence Industry Advisory Council and now Chair of the BusinessNZ Energy Council.

Tina is the Executive Director – Energy and Innovation at BusinessNZ. She leads and manages the BusinessNZ Energy Council (BEC) and is responsible for the development of Business New Zealand policy on all matters relating to energy, transport and innovation. Her work also includes the World Energy Council's Energy Trilemma Framework, Energy Issue Maps and Energy Innovation Framework as well as the content development and organisation of the Asia-Pacific Energy Leaders’ Summit (2016 and 2018) and involvement in the cross-sector BEC Energy Scenarios Projects.

Her fields of specialisation include the energy industry, energy technology, energy policy and marketing.

Prior to her role as Executive Director, she worked as the Senior Policy Advisor for Energy and Innovation at BEC. Tina also worked for enviaM in Germany, a subsidiary of RWE AG, where she was responsible for the purchasing and distribution of electricity and gas. From 2012-2013, she worked in marketing and distribution for STI Solar Technologie International GmbH, Germany. While there, she was responsible for rolling out new products across Europe.

Tina holds a Master of Science (M.Sc.) Value Chain Management from the University of Technology, Chemnitz in Germany and a Bachelor of Arts (B.A.) Management of Energy Utilities from the University of Applied Sciences, Zwickau in Germany, including a semester at the University of Borås in Sweden studying International Marketing and Strategic Marketing.

Energy in New Zealand

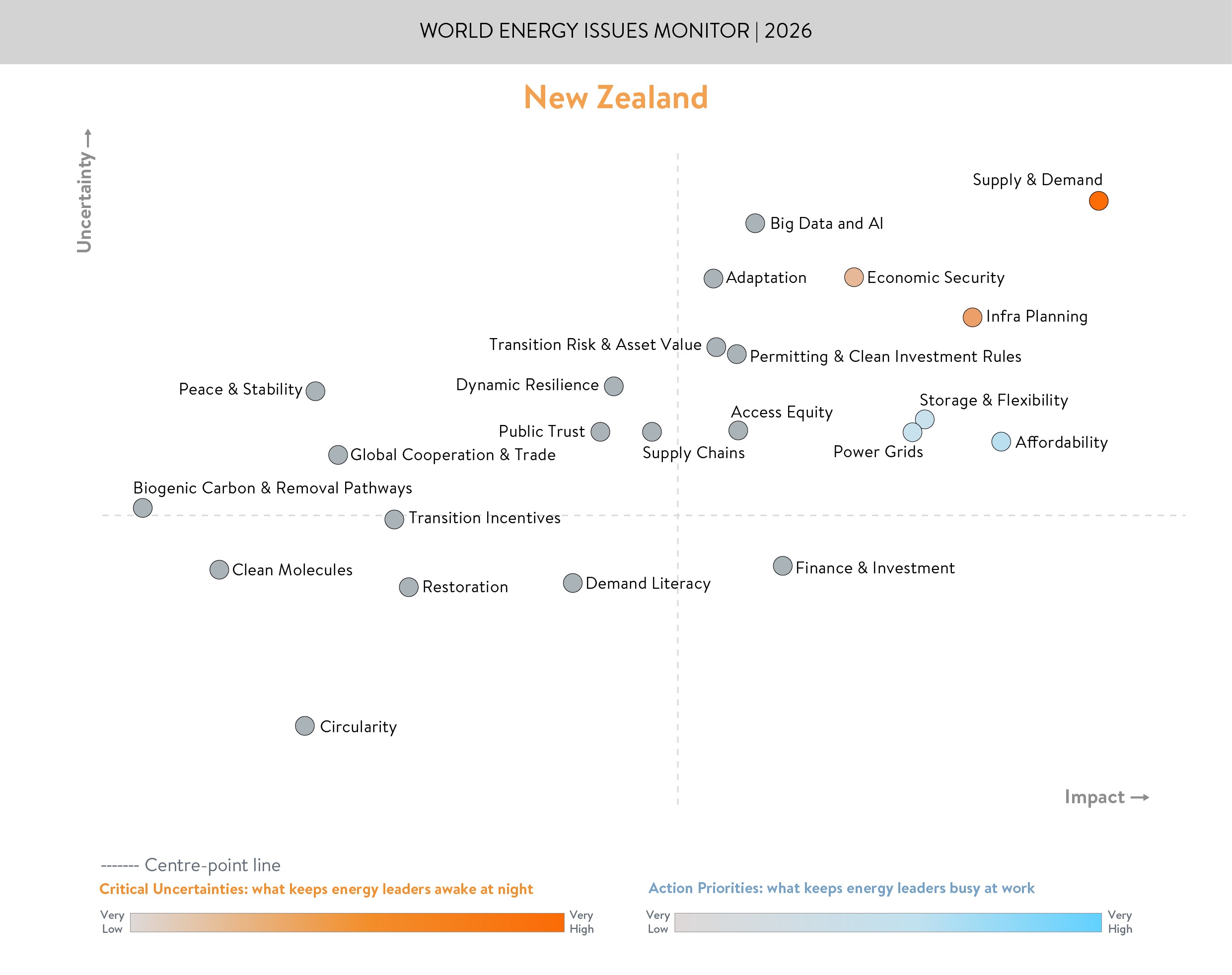

In our 2026 data we have seen significant shifts from our 2025 Issues Monitor results. Affordability is no longer placed as our top Critical Uncertainty but instead is placed as a key Action Priority. This shift signals a greater awareness of the size of the pipeline of electricity generation investment providing a degree of comfort for the future of electricity pricing. Affordability concerns in 2025 remained elevated due to the wholesale price spikes seen in the 2024 dry year. While dry year concerns remain, we did not see the same price spikes in 2025 and through the September-December period wholesale prices remained incredibly low. Affordability remains a key concern within the natural gas sector as our indigenous supply continues to decline, and this is contributing to why we see Supply & Demand as the new top critical uncertainty. 1

Indigenous natural gas production in New Zealand has dropped 35% in the last two years alone and recent work done by our gas regulator indicates that production will half again by 2035. Historically natural gas has underpinned a significant portion of the New Zealand economy, and we are already seeing the demand side impact of reduced supply through business closures and reduction in fuel gas for generation. On the flip side, we are projecting significant electricity demand growth, driven by the electrification of transport, higher demand from commercial and industrial users, and the introduction of data centres. Meeting this demand will be an ongoing challenge for the electricity sector, although encouragingly there is significant investment in new generation.

This demand growth is likely why we see Infrastructure Planning as our second highest critical uncertainty, a shift from what we saw in our 2025 survey where it sat in the middle area of the New Zealand Energy Issues Map. The optimism that we saw last year may have been tempered by questions around how fast projects can actually be permitted, financed and delivered under evolving rules and market conditions. Combined with this, New Zealand’s Infrastructure Commission has found that compared to other countries in the OECD we spend a greater share of GDP on infrastructure but achieve less, which presents a significant challenge. As New Zealand continues to electrify and manage existing assets long term planning is essential.

Economic Security has emerged as our third critical uncertainty mirroring concerns around economic growth last year. Productivity growth has been stagnant in New Zealand for a number of years and with the closure of our only domestic oil refinery in 2022 we are entirely reliant on imports for our engine fuel consumption. We are also becoming increasingly reliant on imported fuel to firm our electricity system as indigenous gas declines. Coal imported from Indonesia has acted as dry year security while the government has publicly announced their intention to build an LNG import terminal, also aimed at meeting dry year risk. Domestic manufacturing capacity is becoming increasingly fragile as energy contracts are more expensive than they have been historically and harder to come by.

TRILEMMA TRADE-OFFS

New Zealand has consistently placed within the top 10 of the Energy Trilemma Index, but the country is now facing renewed discussion on what to prioritise: security, equity or sustainability. Through 2025 we saw record high levels of renewable penetration within our electricity system averaging 96.4% in the October-December 2025 period. However, our renewable heavy system remains vulnerable to dry years where hydro systems cannot run at full capacity.

To meet the challenge of maintaining security of supply through a dry year, the Government has committed to developing an LNG import facility. This trade-off can be represented through the placements of Supply & Demand and Affordability on the New Zealand Energy Issues Map. While affordability has become less uncertain there remains significant concern whether there is enough fuel in the system to maintain Supply & Demand balance when the lakes are low, sun is not shining, and wind is not blowing. LNG is being positioned as a way to ensure that there is enough fuel. The building of the import terminal will be paid via a levy on the electricity industry which will flow through to consumers. The introduction of more imported fossil fuels also creates direct tension when discussing trade-offs between maintaining security of supply and New Zealand’s net-zero commitments.

NEW ZEALAND BLIND SPOTS AND BRIGHT SPOTS

As New Zealand’s energy system changes, we cannot assume continued availability at the scale or price of fuels that have historically been cornerstones of supply. Therefore, it currently seems like key blind spots are Clean Molecules and Biogenic Carbon & Removal Pathways, which currently rank low for perceived uncertainty and impact. This is despite the fact that the development of hydrogen, ammonia and other sustainable biofuels as well as biogenic CO2 and sustainable biomass supply could help to fill the Supply & Demand gaps emerging in our system while also reducing import dependence potentially helping to shift Economic Security away from a critical uncertainty.

The key bright spot to have emerged from 2026 is the significant improvement in the placement of Affordability on the New Zealand issues map. Low hydro levels and a diminishing gas supply had firmly positioned Affordability as our number one critical uncertainty last year, but actions taken by a wide range of stake holders seem to have improved the outlook. Joint industry efforts to create a coal stockpile improved risk management, while industry simultaneously has begun to undergo one of the largest expansions of generation capacity in the country’s history. Government has taken steps to improve market transparency, reduce uncertainty and strengthen energy regulators. Innovation continues with the Government providing funding for super critical geothermal and nuclear fusion, either of which could unlock abundant, clean, secure energy in the longer term.

NEW ZEALAND’S BIGGEST MOVERS

Through the 2025-2026 period New Zealand has seen significant shifts in rankings in its issues monitor. The general trend we have seen is a growth in both uncertainty and impact for the biggest movers. Big Data & AI, Supply & Demand, Public Trust and Access Equity all shifted in this direction. Energy systems are rapidly changing, and these movements reflect that. Data & AI represents a massive driver of energy demand growth which if managed poorly will lead to growing challenges in balancing Supply & Demand. Last year Public Trust was a significant blind spot for New Zealand, and the large movement indicates a shift, acknowledging the importance of public buy-in in facilitating the massive expansion of infrastructure needed. Additionally, as businesses and households are facing increased cost pressures the sector is facing more public scrutiny. Access Equity is becoming a growing concern with energy hardship affecting significant portions of the population. Periods of GDP growth stagnation and in some periods decline, coupled with inflation outpacing wage growth, has put added pressures on household budgets.

Overall, the movements seen between the 2025 and 2026 data acknowledge previous blind spots within the New Zealand energy sector and a growing awareness of the emerging challenges in the country’s rapidly changing energy landscape.

[1] It is worth making a note of changes to the energy landscape since this survey was completed (24 November 2025-12 January 2026) which reinforces Supply & Demand as a top critical uncertainty in New Zealand. As the country is 100% reliant on imported refined fuel, mainly from East Asian refineries, the closure of the Strait of Hormuz has the potential to significantly impact our fuel supply chains. We have already seen the prices of Petrol, Deisel and Jet Fuel rise significantly and there is growing concern around being able to meet demand. These new developments are not reflected in this issues map.

Acknowledgements

New Zealand Member Committee

Downloads

New Zealand World Energy Issues Monitor 2026 Country Commentary

Download PDF

World Energy Issues Monitor 2026

Download PDF

New Zealand World Energy Issues Monitor 2025 Country Commentary

Download PDF

World Energy Issues Monitor 2025

Download PDF

New Zealand World Energy Issues Monitor 2025 Country Commentary

Download PDF

World Energy Issues Monitor 2024

Download PDF

New Zealand World Energy Trilemma Country Profile 2024

Download PDF

World Energy Trilemma Report 2024

Download PDF

Contact the Member Committee

BusinessNZ Energy Council

Level 13, NTT Tower

157 Lambton Quay

Wellington

+64 4 496 6555