Middle East & Gulf States Network

The Middle East and Gulf States region includes major energy producers but also some of the fastest-growing energy consuming countries. The diverse regional community provides national Member Committees and their members with opportunities to expand and deepen their network and engage around activities and events – from young energy professionals to CEO and Ministerial level – on topics of interest to the members.

Regional action priorities that support the Council’s mission and humanising energy vision are agreed on an annual basis by national Member Committees in the framework of a Regional Action Plan. In 2021, key topics of interest to members in the region included the future of hydrogen in the region, the development of a circular carbon economy framework as a comprehensive approach in utilising all available levers for emissions reduction, and conversation about inspirational projects for sustainable energy.

Each month, the Middle East regional network meets to discuss matters of mutual interest, drive collective activities, and keep each other updated on relevant developments and events.

As part of World Energy Week LIVE 2021, a conversation focusing on Circular carbon economy in the Middle East was convened. Participants discussed, how currently mature solutions to address climate change such as energy efficiency and renewable energy are necessary but not be enough to achieve the goals set in the Paris Agreement. They highlighted that in the Middle East and Gulf States, there is a need to develop and deploy technologies of varying maturity to address emissions reductions across multiple sectors. Participants debated how a circular carbon economy framework may provide a comprehensive approach in utilising all available levers for emissions reduction and thereby. address the challenge of climate change while generating socio-economic value by creating valuable products from CO2.

Energy in the Middle East

INTRODUCTION

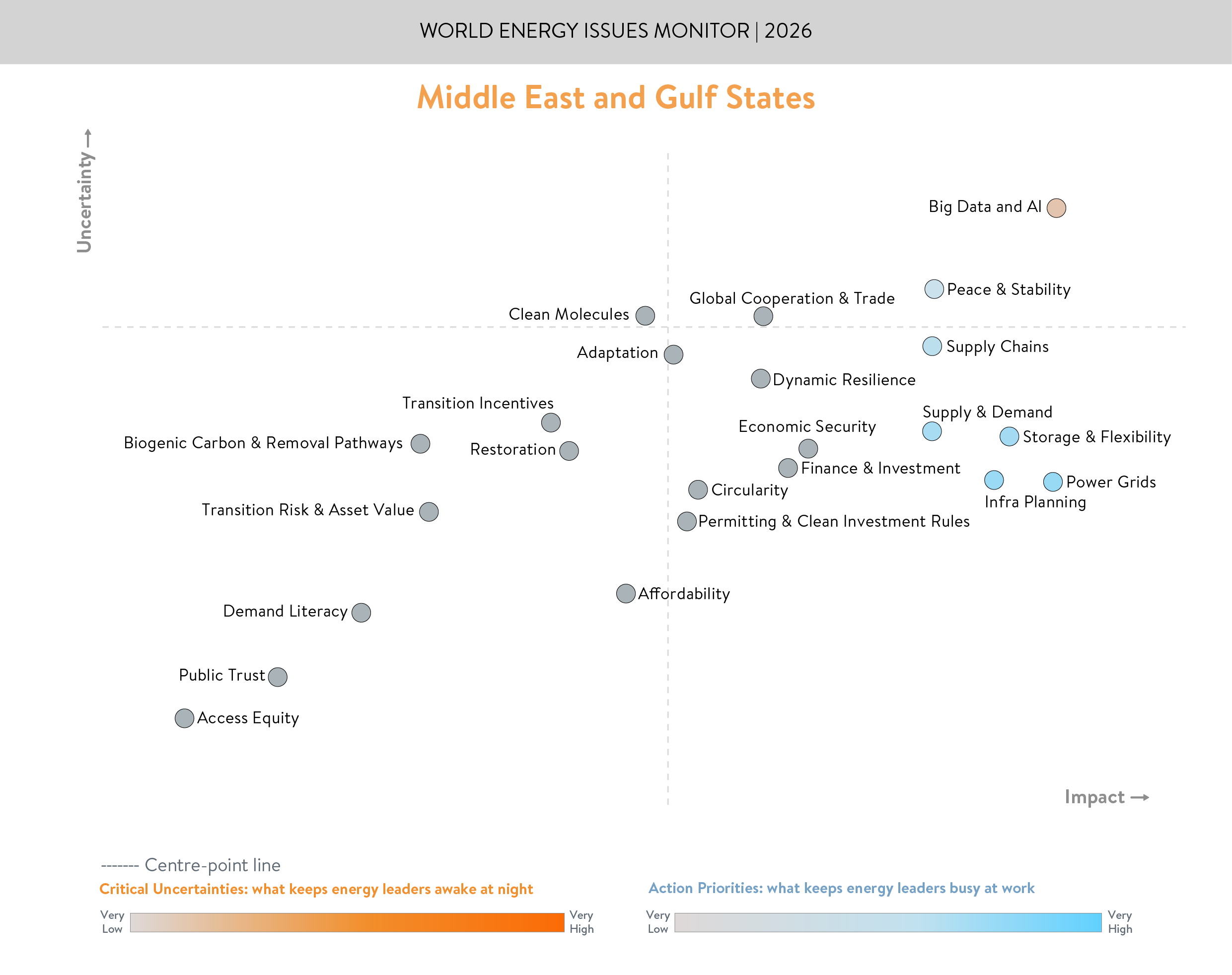

The Middle East & Gulf States (MEGS) Regional Commentary builds on the insights uncovered in this year’s World Energy Issues Monitor, weaving together the region’s leadership dialogue and the pressures shaping its operating environment. The survey and dialogues were conducted prior to the ongoing situation in the region and therefore reflect conditions at that point in time.

The Middle East & Gulf States enter 2026 from a position of strong energy security fundamentals and major investment capacity. Yet the experience of recent years has clarified that energy abundance alone does not guarantee systemic resilience when delivery is increasingly shaped by rapid urbanisation, industrialisation, digital growth, supply chain constraints, and shifting expectations around economic security.

Several 2025 signals reinforced this shift in the region’s operating environment. Surging electricity demand linked to AI and data centres is becoming a material variable for planning, investment sequencing, and system reliability. At the same time, evolving trade dynamics, price volatility across equipment, fuels, and finance, and the growing importance of technology-based economic diversification are changing how energy security is understood. In this context, project bankability and consumer expectations are increasingly shaped not only by resource availability, but also by infrastructure readiness, cost stability, and confidence in delivery.

The region’s transition is becoming more visibly “system-bound” in operational terms. Grid readiness has emerged as a decisive constraint, with connection capacity, long-lead components, and operational redundancies determining how quickly ambition can translate into delivery. The bottleneck has shifted from innovation to implementation: the technologies exist, but deploying them at scale, in parallel, and under compressed timelines is straining institutions, supply chains, and human capital capacity. Operational stress is also becoming more visible, as some systems move beyond reliability concerns toward managing security-of-supply risks and blackout experiences through reactivity and harm reduction.

This is why the Middle East & Gulf States’ 2026 Issues Survey results emphasize this view: constraints are now systemic – rooted in grid readiness, demand growth, supply chain resilience, institutional capacity, human capital, and economic security – rather than a shortage of energy resources or technological solutions.

Under these tighter conditions, the leadership task becomes a World Energy Trilemma-tested delivery: sustaining resource diversification and climate ambition while holding together security, affordability, and sustainability in real time, and ensuring that energy abundance is translated into resilient systems fit for a technology-based economy.

|

ABOUT THE WORLD ENERGY ISSUES MONITOR NOTE ON TIMING AND CONTEXT |

CRITICAL UNCERTAINTIES AND ACTION PRIORITIES

Top Critical Uncertainty: Big Data & Artificial Intelligence (AI)

Big Data & AI has emerged as MEGS' defining uncertainty – reshaping investment decisions, grid planning, siting, and industrial strategy. The question is no longer whether AI demand will grow, but how quickly and unevenly, and with what implications for stability, affordability, and wider development priorities. The Issues Map and regional dialogue reflect a consolidating view: AI-driven load growth is arriving faster than the institutional, infrastructural, and supply chain systems designed to absorb it.

- High ambitions versus delivery headwinds. MEGS countries are pursuing ambitious AI, hydrogen, and clean industry strategies, but ambitions are colliding with bottlenecks: transformer shortages, long procurement cycles, connection delays, and regulatory fragmentation. The uncertainty is whether delivery systems can credibly match the scale and pace of vision. For example, Saudi Arabia's tendering of 64 GW of renewable capacity alongside record-low solar and wind pricing illustrates acceleration of delivery ambition even under volatile global supply chain conditions.

- A regional AI build out race is compressing timelines. Saudi Arabia, the UAE, and others are racing to attract global data centre and AI investment – creating high-density, high-voltage, near-term load that compresses planning and intensifies operational risk. The uncertainty is how systems will prioritise, connect, and stabilise these loads while avoiding congestion and mis-sequencing.

- Resources abundant; allocation contested. Vast oil, gas, and solar potential does not remove uncertainty: allocation does. AI, industry, cooling, mobility, and households are competing for the same electrons and molecules, raising questions about prioritisation and long-term competitiveness. For example, coordinated planning in Saudi Arabia — including efforts to redirect domestic oil towards higher-value uses while reducing liquid fuel use in power generation — is being supported by an extensively metered and increasingly automated grid designed to better manage rising electricity demand and competing system priorities.

- Leading on what – and at what trade-off cost? Strategic identity is in play: leadership in AI, energy exports, low-carbon fuels, system resilience, or diversification each carries opportunity costs – water intensity, grid strain, exposure to external supply chains, fuel displacement, or affordability pressures. Balancing global positioning with domestic 2050 targets remains unresolved. Emerging AI hub ambitions across the region, including large-scale data centre developments in the UAE, further illustrate how digital competitiveness is becoming directly intertwined with power, cooling, and water system constraints.

Top Action Priority: The Delivery Spine – Grids + Flexibility + Responsive Planning

MEGS' transition is now constrained less by technology potential than by system delivery capacity – with grids, flexibility, and coordinated planning setting the pace. Delivery constraints have become systemic: grid capacity, permitting and land processes, supply chain exposure, workforce capability, and institutional coordination must now simultaneously support security, diversification, competitiveness, and resilience.

- Grids are the pacing factor. Grid adequacy – including capacity, connection timelines, and interconnection strength – now determines how quickly MEGS economies can connect renewables and accommodate rising loads from industry, urbanisation, cooling, EVs, and AI/data centres. The binding question is shifting from "what can be built?" to "what can be connected and operated reliably at pace?" Cross-border interconnection (GCC and beyond) is a major accelerator. Saudi Arabia's expansion towards 160,000 km of power lines, alongside interconnection development with Egypt, Iraq, and Jordan, illustrates the scale of grid investment now underway across the region.

- Flexibility and demand management as core system functions. System stability increasingly depends on embedding flexibility – demand response, storage hybrids, managed EV charging, VPPs – and on data-driven visibility (e.g., the UAE's Emirates Monitoring Centre). Without stronger demand-side capability, volatile peak demand and concentrated loads risk overwhelming even well-resourced systems.

- Supply chain resilience as delivery credibility. Price swings in solar and storage, long procurement cycles, component shortages, and global trade reconfiguration are shaping execution. MEGS economies increasingly see localisation not only as an industrial opportunity, but as a strategic resilience lever – using scale, geography, and industrial capacity to reduce external dependency and bring critical value chains closer to deployment.

BLIND SPOTS

- Peace & Stability underweighted relative to real-world influence. Long-standing familiarity with geopolitical turbulence appears to normalise risk on the map, even as it directly shapes investment confidence, supply chain exposure, and security planning.

- Restoration overlooked amid rapid land use and energy expansion. Restoration – protecting ecosystems, biodiversity, and water systems alongside energy expansion – is not treated as a major uncertainty. As renewables, transmission corridors, hydrogen zones, and urban growth areas scale rapidly, cumulative ecological impacts risk eroding long-term resilience and social licence.

- Public trust as a structural delivery variable. Trust rarely appears as high uncertainty, yet transparency, predictable pricing, and stable service are decisive for reforms, siting, and corridor selection. Where trust is not fully established, even well-designed projects stall.

- Access equity as a hidden determinant of approvals and siting. Uneven participation – in lower-income or rapidly changing areas – slows permitting, land access, sequencing, and community acceptance. Without early engagement and equitable benefit sharing, access equity becomes a silent drag on delivery.

BRIGHT SPOTS

- Saudi Arabia: Governance and scale converting ambition into delivery. Unified planning and strong governance are accelerating large-scale grid, gas system, and renewable expansion, with digital asset optimisation identifying approximately 12 GW for new loads such as AI data centres—compressing timelines as demand surges. A centralised planning model, coordinating grid, gas system, and renewable expansion through digital twin technology, is enabling large-scale, synchronised delivery. The Master Gas System expansion, adding 4,000 km of pipeline to displace oil from power generation, and the tendering of over 20 GW of renewables in a single year, illustrate the pace at which governance and planning discipline are converting ambition into physical progress.

- The United Arab Emirates: System leadership under accelerating demand. The United Arab Emirates is consolidating its role as a global reference point for integrated energy system delivery. Real-time system control through the Emirates Monitoring Centre, together with coordinated development across nuclear, solar, hydrogen, interconnection, and the Round-the-Clock clean energy initiative, illustrates a shift from capacity expansion toward continuous, time-matched clean power delivery and shows how system-level speed can be achieved through orchestration rather than build-out alone.

- Lebanon: Decentralised momentum and emerging governance signals. Rapid deployment of distributed solar PV is reshaping electricity access, improving supply reliability for households and businesses while reducing reliance on diesel generation. At the same time, the recent appointment of the Electricity Regulatory Authority marks a long-awaited step toward strengthening sector governance, with the potential to clarify licensing, tariff-setting, and market rules. Together, these developments signal a shift toward a more structured and resilient energy system, where bottom-up adoption is increasingly complemented by institutional progress.

CONCLUSION

Across the region, the task is to sequence delivery under constraint – protecting what works while modernising what blocks throughput. The agenda is delivery over declarations: expand and reinforce grids; accelerate flexibility and demand-side capability; reduce timeline risk through coordinated planning and clear governance; and invest in trust, transparency, and access equity as deliberately as in physical infrastructure.

The goal is Trilemma-tested progress – advancing security AND affordability AND sustainability together, without allowing any single priority to eclipse the others.

Download the full report below.

KEY CONTRIBUTORS

The MEGS commentary draws on insights from across the World Energy Council community, and we are grateful to those who shared perspectives and challenge points that helped sharpen this year’s framing, particularly the Lebanon Member Committee, United Arab Emirates, and Saudi Arabia Member Committee.

Downloads

World Energy Issues Monitor 2026 - Middle East & Gulf States Regional Commentary

Download PDF

World Energy Issues Monitor 2026

Download PDF

World Energy Issues Monitor 2025

Download PDF

World Energy Issues Monitor 2025 - Middle East & Gulf States Regional Commentary

Download PDF

NATIONAL MEMBER COMMITTEES IN THIS REGION

Latest Publications

World Energy Issues Monitor 2026 - What Country Commentaries are Telling Us

Published on 24 June 2026

Practicing Trilemma Discipline – Regional Leadership Exchanges Highlights

Published on 16 June 2026

AI, Data Centres and the Future of Demand – WE Café Discussion Highlights

Published on 16 June 2026

Latest News